News

Indian response on debt structuring, favourable – PMD (Pics)

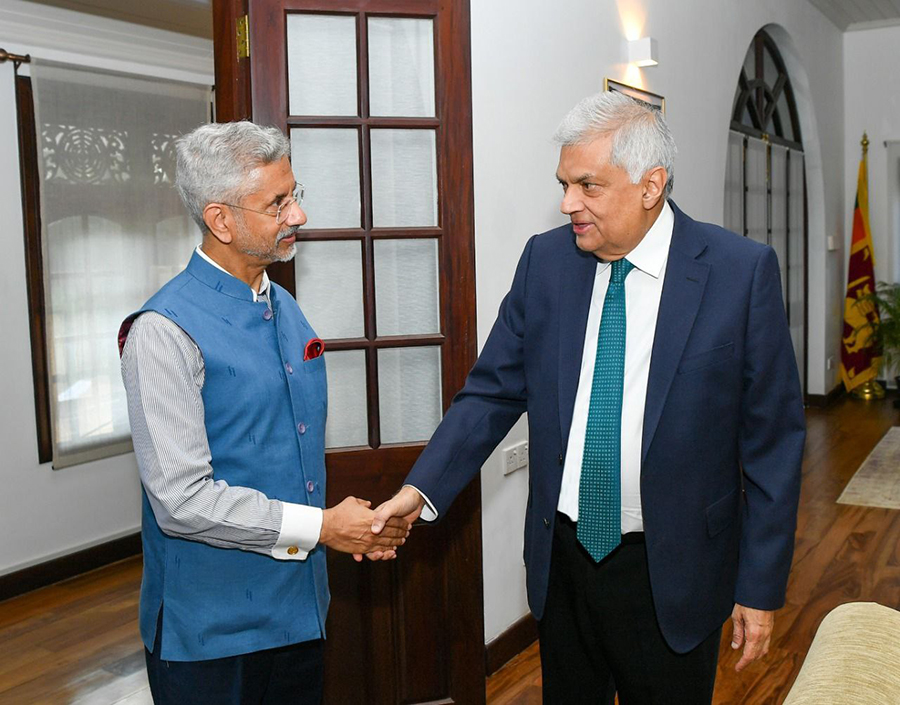

A meeting was held between President Ranil Wickremesinghe and visiting Indian Minister of External Affairs – Dr. S. Jaishankar today, where it was agreed upon to implement a joint program between Sri Lanka and India.

During the meeting, many political, economic and social issues as well as investment matters between the two countries had been discussed at length.

During this discussion, special attention was paid to the debt-restructuring program in Sri Lanka which had received a positive response from the Indian government, the Presidential Media Division (PMD) says.

India and Sri Lanka signed bilateral documents for the upward revision of ceilings prescribed in the High Impact Community Development Project (HICDP) framework agreement today. The agreement, first signed in May 2005, has doubled the individual project limit from Rs 300 to 600 million. The total HICDP funds will be doubled from Rs 5 billion 10 billion.

The President and Dr. Jaishankar also virtually declared open the Academy for Kandyan dancing in close proximity to the Dalada Maligawa in Kandy today, for which Indian PM – Narendra Modi laid the foundation stone during his visit in 2017. Further, 300 completed houses in Galle, Kandy and Nuwara Eliya (100 each) under Indian assistance were also declared open virtually.

The complete media release by the PMD is as follows :

During a meeting held between President Ranil Wickremesinghe and India’s Minister of External Affairs Dr S. Jaishankar, it was agreed upon to implement a joint program between Sri Lanka and India.

President Ranil Wickremesinghe warmly welcomed the Indian External Affairs Minister at the Presidential Secretariat this morning (20) where the duo engaged in cordial discussions.

Prior to the official meeting, President Wickremesinghe hosted the visiting Indian External Affairs Minister Dr Jaishankar for breakfast and tea at his official residence at Paget Road, Colombo.

In addition, in the official meeting held between the President and Indian Foreign Minister Dr S. Jaishankar, many political, economic and social issues as well as investment matters between the two countries were discussed at length.

During this discussion, special attention was paid to the debt-restructuring program in Sri Lanka which had received a positive response from the Indian government.

The Indian External Affairs Minister recalled that in 1991, during the tenure of former Indian Prime Minister P.V. Narasimha Rao, India had to face an economic crisis similar to what Sri Lanka is currently facing. He added that the Indian Government overcame the crisis by pledging the government’s gold reserves.

Therefore, Dr Jaishankar said that India has a good understanding of the situation Sri Lanka is currently facing and said that the Indian government will provide all possible support to solve the current economic problems faced by Sri Lanka.

The bilateral agreement related to raising the limit of the High Impact Community Development Project (HICDP) implemented in Sri Lanka with the support of the Government of India was also signed during the meeting.

The Secretary to the Ministry of Finance, Mr Mahinda Siriwardena, signed the agreement on behalf of Sri Lanka and the Indian High Commissioner to Sri Lanka HE Gopal Baglay signed on behalf of India.

This agreement guides many community development projects in Sri Lanka with the support of the Government of India.

This agreement related to community development projects in Sri Lanka was signed in May 2005. Its project limit was Rs. 300 million, which will now be doubled to Rs. 600 million by the agreement signed today.

Meanwhile, during Prime Minister Narendra Modi’s visit to Sri Lanka in 2017, the foundation stone was laid for the construction of an Academy for Kandyan dancing as a gift given to Sri Lanka by the Indian Government and its people. The Indian Foreign Minister also virtually declared open the academy, which was built near the historical Dalada Maligawa in Kandy.

The handing over of 300 completed houses in Galle, Kandy and Nuwara Eliya – (100 houses each) under the housing project implemented in Sri Lanka with the support of the Indian Government, was also done virtually by the President and the Indian External Affairs Minister.

In this project of 60,000 houses, 50,000 houses have been completed. The third phase of the project of 400 houses for the people of the upcountry estate sector is currently underway and over 3,300 houses built under it have already been completed and are ready to be handed over to the beneficiaries.

The handing over of houses built in Anuradhapura and Badulla districts under the “Model Village Housing Program” implemented with the support of the Government of India for low-income families in Sri Lanka, were also symbolically handed over to the beneficiaries.

Senior Advisor to the President on National Security and Presidential Chief of Staff Mr Sagala Ratnayake, President’s Secretary Mr Saman Ekanayake and other officials and a special Indian delegation attended the discussion.

HNB finance depositors in jeopardy due to ‘PrimeMax’ 0.5% scheme

HNB finance depositors in jeopardy due to ‘PrimeMax’ 0.5% scheme